NEW YORK, 18 MARCH-U.S. manufacturing expanded for the second consecutive month in February 2026, with the ISM® PMI® registering 52.4 percent — a whisker below January’s 52.6, but firmly in expansion territory.

For context, this is only the third expansion reading in the past 40 months, marking a tentative but meaningful turning point for a sector that spent most of 2025 in contraction.

The overall economy has now expanded for 16 straight months, and at 52.4, the PMI corresponds to approximately a 1.7% annualized increase in real GDP — a respectable clip for a heavy industry sector still navigating tariff headwinds and cost pressures.

The Price Shock: Steel, Aluminum, and Tariffs

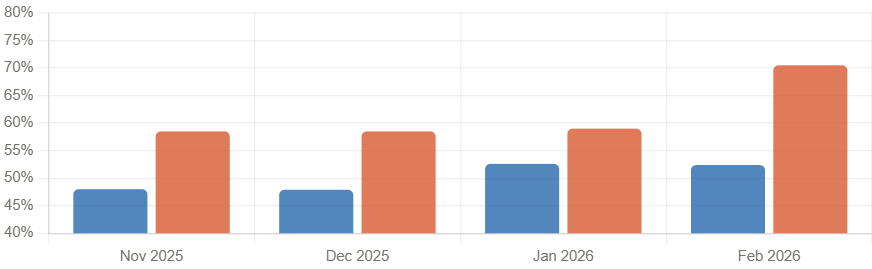

The headline number that will make supply managers and economists sit up is the Prices Index — it catapulted from 59.0 in January to 70.5 in February, an 11.5-percentage-point jump.

That’s the highest reading since June 2022 (78.5%) and signals the most intense cost-inflation in nearly four years.

The culprits are familiar but intensifying: steel and aluminum prices — elevated by Section 232 tariff policy — are rippling through the entire value chain.

One Transportation Equipment respondent put it bluntly: domestic commodities are now the highest-priced in the world, raising costs while simultaneously lowering demand.

The share of respondents reporting higher prices nearly doubled month-over-month, from 29% to 45.4%.

“Today, American produced commodities like steel and aluminum are the highest priced in the world, by far.

Hence, the Section 232 tariff policy is having the exact opposite effect of their intention on an American manufacturer like us: It is raising prices while lowering demand and profitability.”— Respondent, Transportation Equipment sector

Demand Is Real — Orders and Backlogs Both Expanding

Despite cost headwinds, demand fundamentals look solid. The New Orders Index held at 55.8% (down slightly from 57.1 in January), registering a second straight month of expansion after four months of contraction.

For every pessimistic panelist comment, two were optimistic about near-term demand.

More striking: the Backlog of Orders Index surged to 56.6% — up five full percentage points from January — its highest reading since May 2022.

Five of the six largest manufacturing industries expanded their backlogs. This is a forward-looking indicator that bodes well for sustained production in the coming months.

Employment: Still Contracting, But Slowly Recovering

Manufacturing employment remained in contraction for the 29th consecutive month at 48.8%, though the index ticked up 0.7 points from January.

Roughly 45% of panelists indicate that managing headcounts — not hiring — remains the norm, with companies preferring to leave open positions unfilled rather than actively recruit.

There are glimmers of optimism, however.

One Fabricated Metal Products respondent noted a dramatic shift: after spending thousands trying to attract workers with almost no responses over five years, they’ve successfully hired experienced engineers and CNC operators in the last six months.

Which Industries Are Growing?

Twelve of 18 manufacturing industries reported growth in February, while five contracted. The breadth of expansion is notable, spanning from Printing to Computer & Electronic Products.

The Bottom Line

February’s data paints a tale of two manufacturing realities. On the demand side, the picture is encouraging: new orders, backlogs, export orders, and production all expanding, with customer inventories still “too low” — a classically bullish setup for continued output gains.

On the cost side, the picture is increasingly uncomfortable. The Prices Index is flashing its loudest alarm in nearly four years, driven by tariff-inflated metals costs that have no clear near-term resolution.

With 21% of the manufacturing sector’s GDP still in contraction territory in February, the recovery remains uneven.

The key question for Q2 2026: can demand strength outpace the cost pressures long enough to push employment into positive territory? The next reading, covering March 2026 data, releases on April 1.

Also Read

Ohio’s New E-Verify Law Kicks In Tomorrow — How It Could Shake Up Construction Labour

Why Half of All US Home Builders Are Going Broke Without Even Knowing It

- Mulilo pledges nearly R15bn for new renewable energy projects in South Africa - April 2, 2026

- Epiroc Secures Major Order for Autonomous Electric Mining Rigs in Africa - April 1, 2026

- Best Shower Heads for Salty Water:The Complete 2026 Buyer’s Guide to Protecting Your Skin, Hair & Plumbing - April 1, 2026